Sukanya Guha, Data Analyst, Registry Trust

Friday, 3rd February 2023

Following the pandemic related challenges faced by both consumers and businesses, 2022 was likely hoped by many to be a year of recovery. But with the onset of the war and then the cost-of-living crisis, the economy took an unwelcome turn.

At Registry Trust, we maintain the Register of Judgments, Orders, and Fines for the UK & Ireland, which allows us to monitor up-to-the-minute levels of indebtedness and financial vulnerability on an ongoing basis.

The Q4 2022 consumer judgment data has seen a 30% increase year-on-year in the total value of debt. Correlating the judgment data with external datasets can help us to better understand the consumer behaviour during this period of economic crisis.

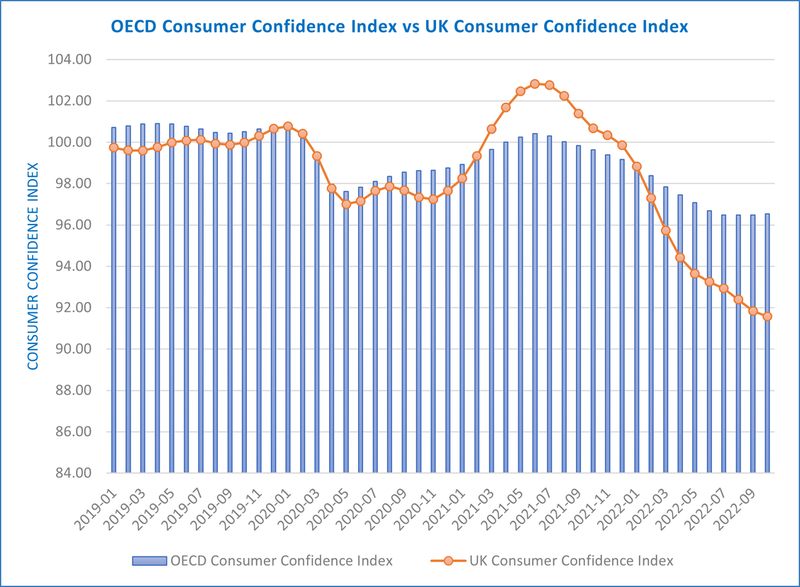

The Consumer Confidence Index (CCI) data published by The Organisation for Economic Co-operation and Development (OECD) is an insightful way to understand current consumer behaviour. The OECD has 38 member countries, the UK being one of them. Analysing the Consumer Confidence Index (CCI) data helps us understand the consumer behaviour in the UK in comparison with the other OECD nations. As seen in the following graph, the UK has a lower value of Consumer Confidence in 2022 compared to the overall OECD index.

Data Source: OECD

According to the OECD, a Consumer Confidence Index (CCI) below 100 indicates a pessimistic attitude towards future development in the economy, possibly resulting in a tendency to save more and consume less. This kind of consumer behaviour was seen during the pandemic in 2020, where we saw a drop in the index due to people spending less and saving more because of Covid restrictions. 2021 witnessed more optimistic consumer behaviour with a Consumer Confidence Index above 100.

However, 2022 has seen the dramatic fall in the Consumer Confidence Index value for the UK, which has previously translated into consumers reducing their spending and instead, saving more. Unfortunately, that’s not what has happened this time. Although Q3 2022 has seen a 9% reduction in discretionary spending according to a report published by Deloitte, the consumers’ savings ratio has also declined in 2022 compared to 2021.

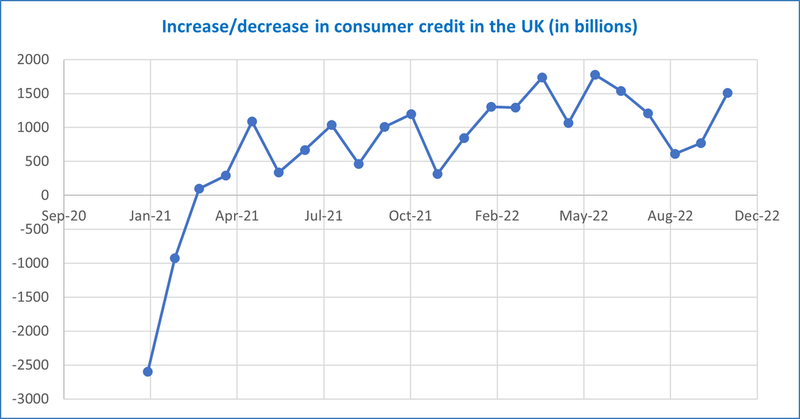

This suggests that consumers are neither indulging in discretionary spending nor saving more. Instead, consumers seem to be exhausting their savings and utilising credit to fund essentials. The following graph highlights the increase in consumer credit in 2022 despite being negative in the start of 2021.

Data Source: https://tradingeconomics.com/united-kingdom/consumer-credit#data

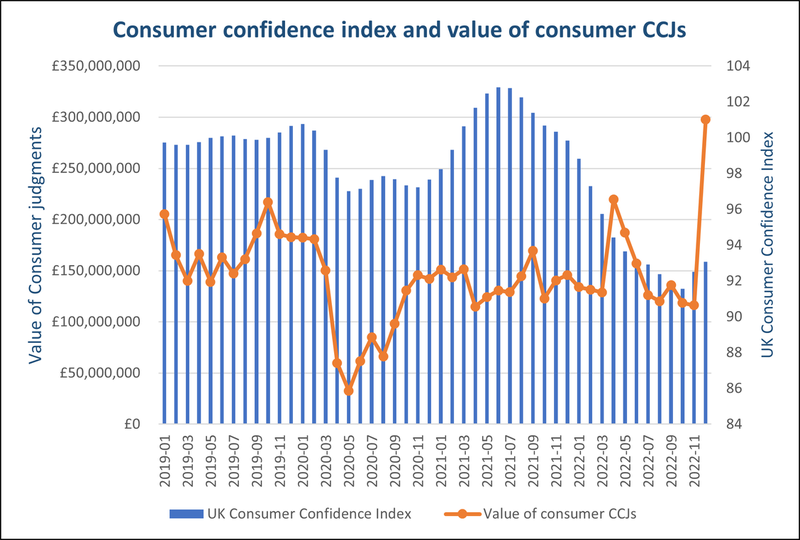

When we layer the UK’s County Court Judgment (CCJ) data on top of the Consumer Confidence Index data, we get the following graph:

Note: UK Consumer Confidence Index plotted solely on the right-hand axis

Previously when Consumer’s Confidence in the economy is low (less than 100), as seen during the pandemic, we have seen a low rate of judgments in that period. But the end of 2022 has seen a completely different picture. In December 2022 there is a dramatic surge of 104% year-on-year in the total value of consumer judgments despite this period having a lower Consumer Confidence Index.

To wrap up our analysis, in an ideal scenario when people spend less they are expected to save more resulting in reduced debt. However, in the present situation, despite sensible spending behaviour, people are exhausting their savings and relying on credit to fund essential spending.