Mick McAteer, Chair, Registry Trust

Thursday, 19th January 2023

There is no question that 2022 was a very tough year for millions of UK households, particularly for those on low or uncertain incomes. Prospects for those households do not look much better for 2023. Registry Trust believes that our data could be better used to develop a more effective response to the cost of living crisis. This paper summarises the perilous state of UK household finances and summarises our key data initiatives.

Financially vulnerable households have lurched from crisis to crisis for over a decade. Earnings have been squeezed, in real terms, since the 2008 financial crisis. Millions of people went into the Covid crisis with wholly inadequate or non-existent levels of financial resilience. The economic effects of Covid were still being felt when households went straight into having to contend with a prolonged cost of living crisis. Economic forecasts suggest little immediate prospect of respite.

Specific interventions will be needed to:

- Help households deal with the ongoing cost of living financial crisis;

- Protect vulnerable households from further financial harm;

- Help affected households repair their finances to ‘get back to square one’; and

- Promote financial resilience against future financial shocks.

Registry Trust does not comment on fiscal, economic, or social policy. It is for government to decide how much financial support should be given to give households. But, as part of our Public Data for the Public Good ethos, we are keen to collaborate with stakeholders to use our existing data resource to better inform and target interventions aimed at protecting financially vulnerable households and small/ micro businesses.

Our data is already an integral part of the data infrastructure which supports hundreds of millions of lending and other business decisions. As well as making better use of our existing data, we also want to enhance our data to help protect consumers and contribute to the challenge of rebuilding household finances and financial resilience. For example, our campaign to increase the number of judgments marked as satisfied[1] on the Register, if successful, could help consumers repair their credit files and access more suitable and affordable products and services. Four and half million people have an outstanding county court judgment (CCJ). Yet, only 16 percent of judgments are marked as satisfied. We are calling for consumer protection regulators to require creditor firms to inform the courts when a CCJ has been satisfied. This is a small change that could make a big difference to many people.

We are also asking government to include the name of the claimant on judgments in England and Wales,[2] not just the defendant as is the case now. This would help consumer protection regulators identify more easily which creditor firms are the most aggressive at enforcing debts and which are treating vulnerable consumers fairly. Our initiative to create a Register of Partial Settlements would benefit consumers who are able to repay part of their outstanding debt. Again, we see this as making a contribution to the challenge of helping houses repair and rebuild their finances.

[1] It is not well known that for a county court judgment (CCJ) to marked as satisfied, it must be settled in full and proof of payment sent to the courts by the defendant. As we explain, below, consumers may neglect to inform the courts with proof of payment, for a number of reasons.

[2] The claimant name is included on the judgment in other UK jurisdictions but not England and Wales, which is the biggest jurisdiction.

THE STATE OF THE NATION’S FINANCES

2022 was a tough year for millions of people

Huge increases in energy prices caused inflation to rise to levels not seen in 40 years. Inflation was a major contributory factor in household disposable incomes falling by over three percent, equivalent to an average of £800 a year per household. This was the biggest annual fall in a century. Three-quarters of households cut back their spending before Christmas 2022.[3] It could have been much worse if it wasn’t for the additional support provided to households by the government.

The Office for National Statistics found that the majority of people (93%) surveyed in recent research reported that their cost of living had increased over the year.[4] The proportion of adults finding it very or somewhat difficult to afford their energy bills, rent, or mortgage payments rose throughout the year. Forty five percent of adults who paid energy bills, and 30 percent paying rent or a mortgage, reported these being difficult to afford.

Of course, different groups of people felt the pressure more intensely. Fifty five percent of disabled adults said they found it difficult to afford their energy bills, compared to 40 percent of non-disabled adults. Sixty nine percent of Black or Black British adults and 59 percent of Asian or Asian British adults said they found it difficult to afford energy bills, compared to 44 percent of White adults. Sixty percent of renters reported finding it difficult to afford their energy bills compared to 43 percent of people with a mortgage. Nearly four in ten (39%) renters reported finding it difficult to afford their rent payments compared to 23 percent of those with a mortgage (but as we highlight below 2023 could be very difficult for mortgagees).

Not surprisingly, people on lower incomes felt the squeeze more than those on higher incomes. Around half of people with an income of less than £20,000 a year reported finding it difficult to afford energy bills compared to under one quarter (23%) of those on £50,000 a year. The situation was even worse for households on prepayment meters. Nearly three quarters (72%) of consumers paying their gas or electricity by prepayment more frequently reported difficulty affording energy compared to 42 percent of those paying by direct debit or in one-off payments. A recent survey by Citizens Advice found that more than 2 million people are being disconnected from their energy supply at least once a month.[5]

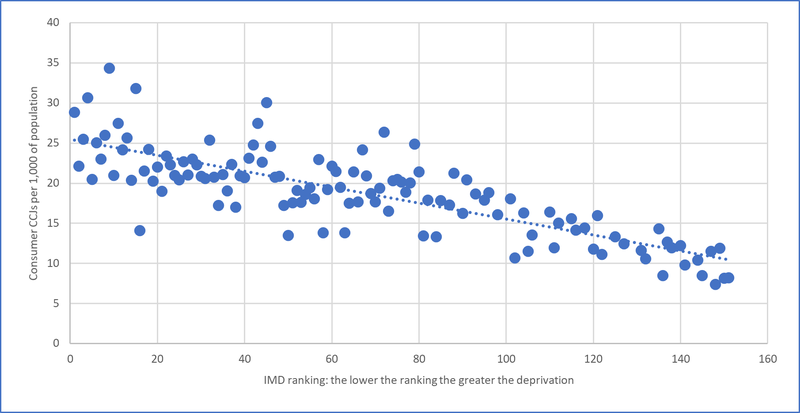

Registry Trust analysis of its local data shows a wide variation in the density of CCJs (as measured by the number of CCJs per 1,000 of the population), and a positive relationship between income deprivation and the density of CCJs. A high rate of CCJs in a local area suggests that there is a higher incidence of problem debt in that area.

In the chart below, the X axis shows the income deprivation ranking.[6] The lower the rank, the more deprived the area. The Y axis shows the CCJ density. The rate of CCJs is 2.5 times higher in the 10 most deprived areas than in the 10 least deprived areas.

[3] New Year's Outlook 2023 • Resolution Foundation

[5] Kept in the dark - The urgent need for action on prepayment meters - Citizens Advice

[6] The Indices of Multiple Deprivation (IMD) combines a number of measures of deprivation such as income and employment deprivation. It is a measure of relative deprivation at a small local area level (Lower-layer Super Output Areas) across England. For this analysis, we use the income domain. See: English Indices of Deprivation 2019 FAQs (publishing.service.gov.uk)

Chart 1: Relationship between income deprivation ranking and density of CCJs in England, 2022

Source: Registry Trust analysis

This is not a recent phenomenon. Registry Trust analysis of 10 years’ worth of its data found a strong positive correlation between higher rates of CCJs and higher levels of over-indebtedness and lower levels of disposable income.[7] Post the 2008 financial crisis, household experiences as measured by CCJ rates, were very different not just between regions but within regions, and between Local Authorities.[8]

Research commissioned by The Health Foundation found a worrying rise in the numbers of adults struggling to afford essential food, goods, and services.[9] In November 2022, 28 percent of adults (14.5 million) reported they could not afford to eat a balanced meal, up from nine percent pre-Covid. Six million adults reported being hungry in the previous month because they couldn’t afford to buy food, more than double the five percent pre-pandemic. Twenty seven percent of adults (14 million adults) said they were unable to adequately heat their homes, up from five percent before Covid. Twenty three percent of adults (12 million adults) said they would not be able to replace electrical goods, up from eight percent before Covid.

The Health Foundation research finds that households are starting to accumulate debts, particularly low-income households. Twenty percent of workers in low income households said their debts had increased moderately or substantially in the previous three months, compared to seven percent of those workers in the equivalent period pre-pandemic. People are increasingly falling behind on bills. One quarter of workers in poorer households have missed at least one priority bill in the previous three months, compared to one in 10 of adults generally.

Charities point to the toll the cost of living crisis is having on our collective mental health.[10] Recent government data reinforces that concern. ONS research undertaken in late 2022 found that 16 percent of adults experienced moderate to severe depressive symptoms, compared to 10 percent pre-Covid.[11] There is a clear regional effect. 25 percent of those who live in the most deprived areas of England were affected by depressive symptoms. Twenty four percent of those reporting difficulty paying their energy bills experienced moderate to severe symptoms compared to just nine percent of those who found it easy to pay bills – that’s nearly three times the rate. Nearly one third (32%) experiencing depressive symptoms said they had to borrow more money or use credit than usual compared to the same period the previous year, with 18 percent of those with no or mild symptoms reporting the same.

The Health Foundation research reports that the mental health of Black and Mixed-race people has worsened by more than other groups between the end of 2021 and 2022. There is an obvious link between lower financial resilience and emotional distress. Nearly three quarters (72%) of those behind in two or more bills feel they are under constant strain compared to 41 per cent of people who are not behind on any bills.[12]

People are turning to borrowing to make ends meet. During 2022, the monthly 12 month growth rate of net credit card lending to individuals (in percent) averaged 11.2 percent. Post the 2008 financial crisis, the average monthly 12 month growth rate was just 3.3 percent.[13]

[7] Analysis presented at Registry Trust AGM 2019

[9] Living-Standards-Outlook-2023.pdf (resolutionfoundation.org), p5/6

[10] Bombarded_policy-note.pdf (moneyandmentalhealth.org)

[11]Cost of living and depression in adults, Great Britain - Office for National Statistics (ons.gov.uk)

[12] Living-Standards-Outlook-2023.pdf (resolutionfoundation.org), for The Health Foundation, p6

[13] Registry Trust analysis of Bank of England data Bank of England | Database Monthly 12 month growth rate of total sterling net credit card lending to individuals (in percent) seasonally adjusted LPMVVUZ

Prospects for 2023 are worrying

If the ghost of Christmas past was frightening, what of the future? The evidence suggests that the situation isn’t going to improve anytime soon. According to the Office for Budget Responsibility, the UK economy is not expected to recover to pre Covid levels until the end of 2024. Inflation will stay high meaning prices will continue to rise (remember, even if the rate of inflation is lower than previously it doesn’t mean prices are falling, just not rising as fast as they were).

The OBR forecasts that by the end of this financial year, 2022-23, real disposable household incomes will have fallen by 4.3 percent. If this happens, it would be the largest fall since the Office for National Statistics (ONS) started collecting records in 1956.

The OBR is then expecting a further 2.8 percent fall in 2023-24, which would be the second biggest fall since records began. So, we are looking at a total fall of around seven percent by the end of the financial year 2023-24 wiping out the income growth we saw in the previous eight years. Indeed, the OBR is expecting that incomes will still be one percent below pre-Covid letters at the end of the 2027-28 financial year.[14]

Overall economic output is still expected to be below its pre-Covid levels by the end of 2024. The energy price guarantee and various cost-of-living support measures had reduced the damage to household incomes by around one quarter. But, this cost-of-living support will be tapered which coinciding with the poor economic outlook does not bode well for financially vulnerable households.

Other analysis supports this gloomy outlook. Rising energy bills, a scaling back of government support, tax rises, and millions of homeowners facing higher mortgage rates (after years of low rates) has led analysts to expect household incomes to take a hit of £880 per household in 2023.[15]

The plight of private renters has been well documented. Homeowners will now be facing higher costs and financial strain, as those with a mortgage will come under pressure now that the protection afforded by very low mortgage rates has begun to be unwound. Over 1.4 million UK households face the prospect of interest rate rises when they renew their fixed rate mortgages in 2023.[16] The Financial Conduct Authority (FCA) has written to the Treasury Committee to warn that more than three quarters of a million households were at risk of defaulting on their mortgage in the next two years.[17]

The cost of living crisis will have longer lasting effects. Lack of savings means people have less financial resilience against future financial shocks. It is likely that many people who do have a financial cushion will continue to dip into their savings to make ends meet next year. The millions of people who already have no, or next to no, savings to rely on are particularly financially vulnerable. Nine million people in the UK have no savings and a further five million have less than £100. Nearly eight in 10 use credit, and 43 percent of those are now anxious about how much they owe.[18]

[14] Office for Budget Responsibility, Economic and Fiscal Outlook, November 2022

[15] New Year's Outlook 2023 • Resolution Foundation

[16] How increases in housing costs impact households - Office for National Statistics (ons.gov.uk)

[18] One in six UK adults have no savings | The Money and Pensions Service

USING DATA TO BETTER TARGET POLICY INTERVENTIONS

How can data help policymakers, regulators, and other stakeholders respond to the millions of households are struggling to cope with a prolonged cost of living crisis.? Analysing data can help us ask searching questions on the nature and scale of problems, provide us with better insights into the factors that cause problems, and shine a light on where the problems are to be found so interventions can be targeted.

As a key producer of economic data, Registry Trust is keen to make better use of our existing data and produce better data to help target policy and regulatory interventions.

There is a need for specific interventions to deal with three interconnected challenges. Households will need support to: cope with the crisis and protection from further financial harm; repair their finances to ‘get back to square one’; and to build financial resilience against future financial shocks.

On the first challenge, financial support and access to independent debt advice will be important in dealing with the cost of living crisis. Interventions might be planned and coordinated centrally but are often best targeted and delivered locally, for example, by local authorities, debt advice agencies, and other third sector organisations. Of course, even the best data cannot be a substitute for ensuring agencies have the appropriate resources to provide financial support and meet the need for debt advice. But, good data can help identify which local areas and communities are in greatest need of support. The granularity and timeliness of Registry Trust’s data can help target resources effectively, especially when combined with other granular data.

It is always important when analysing data to not confuse correlation with causation. Yet, we can say with some certainty that low incomes are not just correlated with high rates of CCJs, they are a significant contributory factor. But, they may not be the only factor. The fact that Chart 1 above shows there is a positive relationship between income deprivation and the density of CCJs at local level is perhaps no great surprise. However, the analysis reveals a significant variation in the CCJ density between areas with similar income deprivation rankings.

Some other factor(s) apart from low income levels must explain this variation. Our previous analysis found that local authorities with high private rents correlate with high rates of CCJs amongst the population.[19] Is it a combination of low incomes and high rents that increases the risk of unsustainable debt? Could it be that in certain local areas, there is a higher concentration of businesses or landlords which are more aggressive in enforcing debt? If so, should policymakers, regulators, and campaigners not be taking an interest? Could it be that local areas with higher CCJ densities have less access to face to face debt advice?

We cannot explain the variation without further investigation. The data should prompt policymakers and other stakeholders to ask questions about whether the most income deprived areas or areas with a large private rented sector have access to the right levels and right type of debt advice. Are financial and other consumer protection regulators using data effectively to map where there are higher concentrations of consumer detriment?

One of the big advantages of Registry Trust data is that it is comprehensive and so allows for robust analysis. The data is available at national, regional, and local authority level going back to 2001. It is also very timely. It is updated daily and we can produce regular analysis to quickly identify trends or where problems are emerging. Timely data on household finances will be critical in helping policymakers, regulators, and civil society respond to the cost-of-living crisis.

We know policymakers and stakeholders could make better use of existing, available data produced by Registry Trust to target interventions. But, what about producing better, new data?

There is no question that helping households deal with the ongoing cost of living financial crisis and protecting them from further financial harm is the immediate priority. However, we cannot just continue dealing with crises, we should also think about how pre-empt and prevent future problems. This means helping affected households repair their finances to ‘get back to square one’ and promote financial resilience against future financial shocks. We want to help build a bridge to financial inclusion.

There are a number of initiatives that we are working on which would further enhance the utility of our data for policymakers, regulators, and civil society. The proposals are to:

- address the problem of county court judgments (CCJs) not being marked as ‘satisfied’ on the public register;

- to include the name of the claimant on the public register; and

- create a partial settlements register.

Satisfactions

We estimate that 4.5 million consumers and small/ micro businesses have at least one outstanding CCJ debt. CCJ data, as well as being a lagging indicator (in that a CCJ is enforced when arrears and debts have not been managed), can be a leading indicator of consumers’ ability to access affordable products and services. A CCJ stays on the Register for six years so this can affect consumers’ ability to access affordable credit and insurance in the future. This makes them financially vulnerable in the future. So, it is very important from a consumer rights perspective that information held on the Register is a true and up to date record of a consumer’s financial position. But, there are wider implications. CCJs are also used by landlords and employers so this can affect more than consumers’ rights of access to affordable credit.

Yet, currently, just 16 percent of CCJs are marked as ‘satisfied’ on the Register, and this proportion has been falling over time. It is not well known that for a CCJ to marked as satisfied, it must be settled in full and proof of payment sent to the courts by the defendant. Consumers may neglect to inform the courts with proof of payment, for a number of reasons, not least because of the stress and anxiety caused by having to deal with problem debts. People in debt can face a vicious circle of mental health issues making it more difficult to manage finances, while getting into financial difficulty can exacerbate mental health issues. At times of severe stress and anxiety, understanding that there is yet another step to take of having to remember to inform the courts and sending proof of payment can be difficult.

Whatever the reason, many consumers who have already repaid their outstanding debt could still be penalised if the CCJ has not been marked as satisfied. This problem could be addressed in a number of ways. The most effective way would be for regulators to introduce a rule or issue guidance to firms within their remit to notify the courts when a debt has been settled. This should be seen as part of a firm’s treating vulnerable consumers fairly obligations. Notification could be done by email on receipt of settlement of the debt so would not impose any difficult requirements on firms.

Notifying the courts that a debt has been repaid would not be onerous for firms. It would be a very simple step that could have a big impact. It would show that firms are taking all reasonable steps to support vulnerable consumers through what can be a very difficult period in their lives. It could also help consumers repair their credit files and household finances, and recover more quickly from a difficult financial position. Improving the information on the register could enable access to more suitable and affordable products and services. Overall, we think this could contribute to the challenge of rebuilding of household finances post the cost of living crisis.

[19] The impact of Universal Credit uplift on renting and CCJ debt in England (registry-trust.org.uk)

Claimant data

Registry Trust has been asking government to include details of the claimant as well as the defendant on judgment records. As it stands, we can publish the name of the claimant for Scotland and Northern Ireland judgments but not for England and Wales, which is by far the largest jurisdiction. Including the name of the claimant on the Register would be another small step that could have a big impact. It could be an effective consumer protection tool for regulators.

If the Register held the name of the claimant, regulators could use this real time data to monitor how regulated firms treat consumers in a vulnerable financial position, particularly important given the ongoing impact of the cost of living crisis. It would allow regulators to identify detrimental practices and respond more quickly. Regulators could spot which firms within their remit are most aggressive in using enforcement action, and compare their stated treating customers fairly policies against their actual practices. It could also provide a helpful indicator of the quality of controls lenders have in place to prevent irresponsible lending or, for utilities and telecoms providers, the effectiveness of policies intended to support consumers in financial difficulty.

Claimant data could also be a helpful corporate accountability tool for civil society groups. It would also help academics and other analysts obtain better insights into the source of problem debt within the economy. It could also be a useful input for determining the funding of debt advice based on the harm caused. Including the claimant name on the public register would help government, the Money and Pensions Service (MaPS) and other stakeholders identify with more precision which activities, sectors, and firms are responsible for causing financial problems for consumers.

A register of partial settlements

As mentioned above, there are 4.5 million individuals and small/ micro enterprises with at least one outstanding CCJ, either because they have not been paid in full or been paid but not formally marked as ‘satisfied’ within the six years since being issued. Within this 4.5 million there are consumers who have made a partial payment of an outstanding debt which the creditor has accepted as a settlement.[20]

However, as the amount paid is less than the recorded debt on the CCJ, there is currently no requirement or process in place for the CCJ record to be amended on the Register. This means that even though the creditor has accepted a partial payment as a settlement, and in the eyes of both parties the debt has been settled, it remains as fully outstanding on the Register and on the consumer’s credit file.

The CCJ record therefore does not fully reflect the true financial position, and this can have a knock-on impact on lending and other business decisions made using our data. The result is that there is little financial incentive for consumers to make a partial payment, which is not in creditors’ interests either. It also seems unfair that consumers, who have tried to repay at least some of an outstanding debt, do not get recognition for this.

To address this, we are hoping to create a Register of Partial Settlements, in conjunction with stakeholders from both the credit information and debt advice industries. We think this would benefit consumers who are able to repay part of their outstanding debt, while protecting the interests of those who cannot afford to make a partial payment. Again, we see this as making a contribution to the challenge of helping houses repair and rebuild their finances.

[20] This might happen when a CCJ is issued based on a ‘misunderstanding’. For example, a tenant might have moved house without a water company having a record of it – both parties may settle the debt for the duration of the tenancy which is less than the amount for which the CCJ is recorded.

CONCLUSION

The various surveys produced recently paint a very bleak picture. 2022 was a very tough year for millions of UK households, particularly for those on low or uncertain incomes. Millions are facing serious levels of financial stress. Prospects for these financially vulnerable households do not look much better for 2023. Improvements will only be seen if we are able to make the crucial interventions suggested to protect consumers from financial harm; to help households repair their finances and to promote financial resilience for the future.

As part of our Public Data for the Public Good ethos we are keen to collaborate with stakeholders to use our existing data resource to better inform and target interventions aimed at protecting financially vulnerable households. We know that better data usage and understanding will help us contribute to the challenge of rebuilding household finances and financial resilience.

We look forward to working with stakeholders to develop ways to use data to make better policy.

Contact: business@registry-trust.org.uk