Millie Corless, Data Analyst, Registry Trust

Monday, 20th September 2021

The link between commercial CCJs and insolvency: From first judgment to insolvent in 999 days

The unfortunate reality of receiving a commercial County Court Judgment (CCJ) is reduced access to credit and borrowing, which can be detrimental to a business’ survival.

At Registry Trust, we maintain the Register of Judgments, Orders, and Fines for the UK & Ireland which gives us access to a live indicator of indebtedness for both businesses and consumers. We use this ‘public data for public good’ and often analyse it against other relevant datasets to identify economic and social trends which may be useful in informing policy, research, and public education.

In July 2021, we obtained two months’ worth of commercial insolvency sample data (May & June 2021) from The Gazette (which provides the official public record of important statutory and non-statutory notices including commercial insolvency data). I was able to match some of this data to our data from the Register to investigate whether there was a link between a company having CCJ(s) against them and later becoming insolvent. I wanted to find out if a commercial CCJ is an early indicator of insolvency so that this information could be used to support businesses that are at risk. One of the services Registry Trust provides is ‘Special Request’ data for debt management and insolvency companies to help them identify prospects to offer business rescue support to. Our hope is that understanding the link between commercial CCJs and insolvencies might help these organisations to better identify and support companies at an earlier stage to try and avoid insolvency.

In the analysis of our data and the Gazette data from May and June 2021, I matched 39 companies which had received 133 CCJs (or other type of commercial monetary judgment) in the past six years. Five judgments and two companies were removed from analysis due to discrepancies in the data. This left 37 companies matching to 127 judgments. This is a matching rate of almost half (47%) from the original 79 businesses who became insolvent from May to June 2021.

One particularly interesting – and concerning – finding was that, of the 37 companies, eight (22%) became insolvent after just one judgment against them, with the average number of days between judgment and insolvency equalling 605.8 days, or 19.5 months. Given that a CCJ or other type of monetary judgment is usually a last resort after trying to recover arrears by other means, it is likely that the companies receiving them are already in some sort of difficulty, hence why it may be a pathway to insolvency.

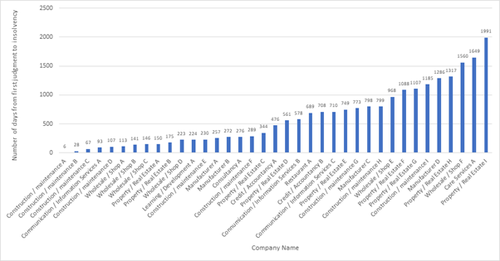

The number of days from first judgment to insolvency for the 37 companies (29 of which received more than one judgment) is shown in the graph below with anonymised company names categorised into sectors. ‘Construction/maintenance company A’ entered into insolvency only six days after receiving its first judgment. ‘Property / Real Estate company I’ took the longest number of days to become insolvent following its first judgment: 1,991 days.

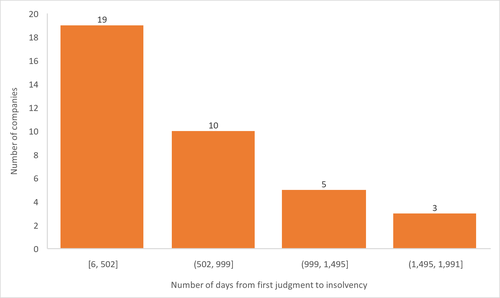

Division of the 1,991 days (the maximum number of days a business took to become insolvent after their first judgment) into four quarters shows 19 companies fell into the first quarter (becoming insolvent within 502 days), and 10 into the second quarter (becoming insolvent between 502 and 999 days). This means that 78% of businesses in this study became insolvent within 999 days of their first judgment.

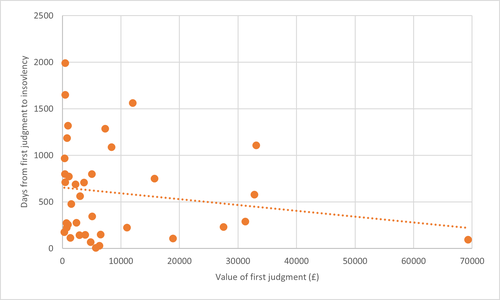

There is also a positive correlation between the value of a judgment and time taken for a business to become insolvent. The graph below shows that, as the value of the first judgment increases, the number of days between first judgment and insolvency decreases. It is worth noting that this does not account for the number of judgments a business may have received.

This is vitally important information, particularly for small businesses who may be more susceptible to financial decline given a sudden financial shock. Judgments remain on the Register for six years, and the disadvantages that having a judgment brings to a business makes it vital to get them resolved as quickly as possible, whether that is by repaying the debt within one calendar month to prevent it appearing on the Register (and therefore on the company’s credit file/our public-facing website TrustOnline where anyone can check if a business has an outstanding CCJ) or by settling and, most importantly ‘satisfying’, it so that it shows as paid on the Register. The ‘Help Topics’ on our TrustOnline website has more information for consumers and businesses about dealing with CCJs.

Find out more about uses of our data and working with us in our downloadable e-brochure here.

To keep up to date with the latest from Registry Trust, click here to subscribe to our monthly updates and/or follow us on Twitter and LinkedIn. You can also follow our public website TrustOnline on Facebook and LinkedIn for regular useful updates about CCJs, credit scores and more.